CPA Guide: 5 Steps to Build a Profitable Tax Advisory Firm

Discover how forward-thinking accounting firms are transforming from reactive tax preparation to high-margin advisory services—and generating 40-60% more revenue per client.

The Paradigm Shift: From Compliance to Advisory

The accounting profession stands at a crossroads. Traditional tax preparation services face mounting pressures:

- Commoditization through DIY software like TurboTax and H&R Block’s digital platforms

- Price compression as automated solutions undercut hourly rates

- Seasonal volatility creates feast-or-famine cash flow cycles

- Declining margins on standard compliance work

- Client perception as transactional vendors rather than strategic partners

Meanwhile, proactive tax planning services command premium pricing, generate recurring revenue, and position CPAs as indispensable business advisors. Firms successfully making this transition report:

- 2-3x higher revenue per client compared to compliance-only relationships

- Reduced seasonality through year-round advisory engagements

- Improved client retention rates exceeding 95%

- Higher practice valuations when selling or transitioning ownership

- Enhanced job satisfaction for staff and partners

This comprehensive guide reveals how to transform your CPA practice from a seasonal tax shop into a strategic advisory powerhouse.

Why Proactive Tax Planning Is the Future of Accounting

The Financial Case for Tax Advisory Services

Traditional Tax Preparation Model:

- Average client value: $800-1,500 annually

- Service delivery: 3-4 months per year

- Client engagement: Reactive, compliance-focused

- Revenue predictability: Highly seasonal

- Competitive differentiation: Limited

Proactive Tax Planning Model:

- Average client value: $3,000-8,000+ annually

- Service delivery: 12 months per year

- Client engagement: Strategic, relationship-focused

- Revenue predictability: Consistent monthly recurring revenue

- Competitive differentiation: Significant

What Clients Actually Want (And Will Pay For)

According to theCPA.com 2024 Tax Planning Survey, 73% of business owners want proactive tax planning advice, but only 31% receive it from their current accountant.

The gap represents a massive opportunity. Clients are actively seeking:

- Tax reduction strategies that minimize liability legally and ethically

- Cash flow optimization aligned with tax obligations

- Entity structure planning as businesses grow and evolve

- Succession and exit planning, maximizing after-tax proceeds

- Real estate tax strategies for investors and operators

- Retirement planning integration combining tax and wealth management

- Estimated tax management avoiding penalties and surprises

Business owners consistently report willingness to pay 3-5x more for strategic tax planning versus basic preparation services—yet most CPAs continue offering only the latter.

The Six Pillars of Proactive Tax Planning Services

1. Strategic Entity Structure Analysis

Why It Matters:

Business entity selection dramatically impacts tax liability, asset protection, and operational flexibility. Yet many businesses operate in suboptimal structures due to:

- Inertia from initial formation decisions

- Lack of awareness about alternatives

- Missing opportunities to adapt as revenue scales

Advisory Opportunities:

S-Corporation Elections for Sole Proprietors

- Potential self-employment tax savings: $5,000-$15,000+ annually

- Reasonable compensation analysis and documentation

- Quarterly distribution planning

LLC to C-Corporation Conversions

- Accessing Qualified Small Business Stock (QSBS) benefits

- Section 1202 exclusion allowing up to $10M tax-free gain

- Strategic timing for venture-backed companies

Partnership vs. Multi-Member LLC Considerations

- Pass-through treatment optimization

- Basis tracking and planning

- Special allocation opportunities

Holding Company Structures

- Asset protection through separation

- Tax-efficient profit distribution

- Estate planning integration

Implementation Process:

- Analyze current structure and historical tax returns

- Model alternative scenarios with 3-5 year projections

- Calculate transition costs and breakeven timeline

- Coordinate with legal counsel for implementation

- File elections and structural documents

- Establish an ongoing compliance calendar

Revenue Opportunity: $2,500-$7,500 per entity restructuring project

2. Multi-Year Tax Projection and Scenario Planning

Why It Matters:

Single-year tax preparation offers zero visibility into future obligations. Proactive planning requires looking forward to:

- Anticipate income fluctuations and plan accordingly

- Time major transactions for optimal tax treatment

- Harvest losses strategically before expiration

- Maximize deductions before phase-outs occur

- Plan for estimated tax obligations, avoiding penalties

Advisory Opportunities:

Three-Year Tax Forecasting

Develop comprehensive projections incorporating:

- Expected business revenue growth or contraction

- Planned major expenditures (equipment, real estate, expansions)

- Anticipated life events (marriage, divorce, inheritance, retirement)

- Investment transactions and portfolio rebalancing

- Stock option exercises and equity compensation events

Scenario Modeling

Create “what-if” analyses for client decision-making:

- “Should I buy or lease this $150,000 equipment?”

- “What are the tax implications of selling my business this year vs. next?”

- “How does hiring my spouse as an employee affect our taxes?”

- “Should I take this distribution now or defer until next year?”

Quarterly Tax Review Meetings

Implement structured touchpoints:

- Q1 (January-March): Tax return review and prior year analysis

- Q2 (April-June): Mid-year projection update and estimated tax adjustment

- Q3 (July-September): Third quarter check-in and planning opportunity assessment

- Q4 (October-December): Year-end planning and implementation deadline

Tools and Technology:

Modern tax planning requires sophisticated software:

- Corvee Tax Planning – Comprehensive scenario modeling

- Holistiplan – Tax planning for financial advisors

- BNA Income Tax Planner – Bloomberg’s projection software

- Excel-based custom modeling tools

Revenue Opportunity: $3,000-$6,000 annual retainer per client

3. Cost Segregation and Depreciation Acceleration

Why It Matters:

Real estate investors and business owners with significant property holdings often leave substantial tax savings on the table by:

- Using default straight-line depreciation (27.5 or 39 years)

- Missing cost segregation study opportunities

- Failing to maximize Section 179 and bonus depreciation

Advisory Opportunities:

Cost Segregation Studies

Identify and reclassify building components into shorter recovery periods:

- Typical building: 27.5-39 year depreciation

- After cost segregation: 30-40% of cost reclassified to 5, 7, or 15-year property

- Immediate benefit: Massive first-year deductions through bonus depreciation

Example Impact: $2M commercial building purchase

- Traditional depreciation: ~$51,000/year

- After cost segregation: $600,000-800,000 first-year deduction

- Tax savings: $150,000-$250,000 (assuming 35% effective rate)

Section 179 Optimization

Strategically deploy immediate expensing:

- 2025 limit: $1,220,000 for qualifying property

- Phase-out threshold: $3,050,000 in purchases

- Coordinate with bonus depreciation for maximum benefit

Tangible Property Regulations Planning

Advise on repair vs. capitalization decisions:

- De minimis safe harbor elections ($2,500 or $5,000)

- Routine maintenance safe harbor

- Building improvement distinction (roof, HVAC, structure)

Qualified Improvement Property (QIP) Strategy

Leverage a 15-year recovery period for interior improvements:

- Bonus depreciation eligibility

- Significant acceleration for tenant improvements

- Restaurant and retail renovation opportunities

Implementation Requirements:

- Identify eligible properties and projects

- Engage a qualified cost segregation specialist

- Review engineering reports and classifications

- File appropriate tax forms and elections

- Update depreciation schedules and fixed asset records

- Document decision rationale for audit protection

Revenue Opportunity:

- Referral fees from cost segregation firms: 10-20% of the study fee

- Tax planning integration: $1,500-$3,500

- Ongoing depreciation management: Included in annual service fee

4. Retirement Plan Design and Contribution Strategies

Why It Matters:

Retirement plan contributions offer:

- Immediate tax deductions reduce current liability

- Tax-deferred growth accumulation

- Asset protection benefits in most states

- Estate planning and wealth transfer opportunities

Yet many business owners contribute far less than optimal amounts due to:

- Lack of awareness about contribution limits

- Misunderstanding of available plan types

- Missing opportunities for profit-sharing allocations

- Failure to integrate with overall tax planning

Advisory Opportunities:

Plan Design Analysis

Evaluate whether the current plan maximizes tax savings:

Solo 401(k) for Owner-Only Businesses

- 2025 contribution limits: $70,000 ($77,500 age 50+)

- Combines employee deferrals and profit-sharing

- Allows mega backdoor Roth contributions

- No discrimination testing required

SEP-IRA for Simple Administration

- Contribution limit: 25% of compensation (20% for self-employed)

- Maximum: $70,000 for 2025

- No annual filing requirements

- Flexible year-to-year contributions

Defined Benefit/Cash Balance Plans

- Contribution potential: $100,000-$350,000+ annually

- Ideal for high-income professionals age 45+

- Predictable income projection required

- Higher administrative complexity and cost

Safe Harbor 401(k) Plans

- Avoid discrimination testing

- Maximize owner contributions regardless of employee participation

- Required employer contribution (3% or 4% match)

Strategic Contribution Timing

Optimize when contributions occur:

- December vs. January timing for cash flow management

- Prior-year contributions before tax deadline (SEP-IRA/Solo 401(k))

- Coordinating with estimated tax payments

- Bunching contributions in high-income years

Roth Conversion Planning

Strategically move traditional retirement funds to Roth:

- Identify low-income years for conversions

- Multi-year laddered conversion strategies

- Balance with bracket management

- Coordinate with other tax planning opportunities

Backdoor and Mega Backdoor Roth Strategies

Navigate contribution limit restrictions:

- Traditional IRA contribution followed by Roth conversion

- After-tax 401(k) contributions converted to Roth

- Pro-rata rule considerations and planning

- Documentation and compliance requirements

Revenue Opportunity: $1,500-$4,000 annual planning + 10-15% of plan administration fees (if offered)

5. Business Expense Optimization and Documentation

Why It Matters:

According to IRS data, small businesses average only 60-70% of legitimate deductible expenses on their returns, leaving substantial tax savings unclaimed due to:

- Poor recordkeeping and documentation

- Lack of awareness about allowable deductions

- Fear of audit triggering “red flags”

- Missing home office, vehicle, and travel deductions

- Inadequate substantiation for meals and entertainment

Advisory Opportunities:

Home Office Deduction Maximization

Most home-based business owners either:

- Don’t claim it at all (fear of audit)

- Use a simplified method, leaving money on the table

Strategies:

- Actual expense method calculation and comparison

- Direct vs. indirect expense allocation

- Depreciation recapture planning for future sale

- Administrative office vs. principal place of business qualification

Vehicle Expense Planning

Choose optimal method and maximize deductions:

Standard Mileage Rate (2025: $0.70/mile)

- Simpler recordkeeping requirements

- Often better for older, lower-value vehicles

- Can switch to actual method in future years

Actual Expense Method

- Detailed tracking of all vehicle costs

- Depreciation and Section 179 opportunities

- Better for expensive vehicles with heavy business use

- Cannot switch back to standard mileage

Section 179 Vehicle Strategy

- Vehicles over 6,000 lbs (SUVs, trucks) qualify for full expensing

- Luxury vehicle limits: $12,200 first year (2025)

- Coordinate with bonus depreciation

- Heavy vehicle strategy for real estate and construction businesses

Meal and Entertainment Substantiation

Navigate complex deductibility rules:

- 50% deductible: Most business meals

- 100% deductible: Employee meals (de minimis fringe benefit)

- 0% deductible: Entertainment expenses (post-TCJA)

- Documentation requirements: Who, what, when, where, business purpose

Travel Expense Optimization

Maximize deductions for business travel:

- Per diem vs. actual expense methods

- Combining business with personal travel

- Convention and seminar qualification rules

- Spouse travel deductibility criteria

- Documentation and substantiation requirements

Equipment and Technology Purchases

Strategic acquisition timing:

- Section 179 immediate expensing ($1,220,000 limit 2025)

- Bonus depreciation (currently 60% in 2025, decreasing annually)

- Year-end purchases for full-year depreciation

- Trade-in vs. sale considerations

Health Insurance and Medical Expense Planning

Optimize healthcare-related deductions:

- Self-employed health insurance deduction (above-the-line)

- Health Savings Account (HSA) strategies ($4,300 individual, $8,550 family 2025)

- Health Reimbursement Arrangements (HRAs) for S-corp owners

- Medical expense itemized deduction threshold (7.5% AGI)

Accountable Plan Implementation

For employers reimbursing employee expenses:

- Establish a written accountable plan policy

- Substantiation and return of excess requirements

- Exclude reimbursements from W-2 wages

- Deduct expenses at the corporate level

Revenue Opportunity: Included in comprehensive tax planning retainer; specialized expense optimization audit: $1,200-$2,500

6. Tax-Loss Harvesting and Capital Gains Management

Why It Matters:

Investment portfolio management intersects with tax planning to:

- Offset capital gains with strategic losses

- Optimize long-term vs. short-term treatment

- Plan for low-tax-bracket years

- Coordinate with business exit and sale events

Advisory Opportunities:

Strategic Tax-Loss Harvesting

Systematically identify opportunities to:

- Harvest losses in declining positions

- Offset short-term gains (taxed up to 37%)

- Carry forward excess losses ($3,000 annual limit)

- Avoid wash sale rule violations (30-day restriction)

Capital Gain Bracket Management

Carefully manage income to optimize rates:

- 0% bracket: Taxable income under $96,700 (married filing jointly 2025)

- 15% bracket: $96,700-$600,050

- 20% bracket: Over $600,050

- Net Investment Income Tax (NIIT): Additional 3.8% over threshold

Strategies:

- Defer income into future years when expecting lower brackets

- Accelerate income when temporarily in lower brackets

- Time asset sales around other income fluctuations

- Coordinate with retirement account distributions

Qualified Small Business Stock (QSBS) Planning

Maximize Section 1202 exclusion benefits:

- Potential exclusion: Up to $10M or 10x basis

- Requirements: C-corporation, $50M gross assets at issuance, 5-year holding period

- Qualifying business definition

- Stock acquisition timing and documentation

Opportunity Zone Investment Strategy

Leverage a tax-deferred investment vehicle:

- Defer capital gains through December 31, 2026

- Partial gain exclusion if held 5+ years (10% basis step-up)

- Complete exclusion of appreciation if held 10+ years

- Qualification requirements and eligible investments

1031 Exchange Facilitation

Defer real estate capital gains:

- Like-kind exchange requirements

- 45-day identification period

- 180-day closing deadline

- Reverse exchange and improvement exchange variations

- Qualified intermediary coordination

Installment Sale Planning

Spread the gain recognition over multiple years:

- Seller financing creates an installment sale

- Interest income vs. principal allocation

- Minimum interest rate requirements

- Depreciation recapture treatment

Revenue Opportunity: Coordination fee: $1,500-$3,500; Ongoing portfolio tax planning: 0.10-0.25% of AUM

Building Your Tax Planning Service Model

Packaging and Pricing Strategies

Tiered Service Offerings

Create clear value propositions at multiple price points:

Bronze Tier – “Essential Tax Planning”

- Annual tax return preparation

- One mid-year tax projection

- Basic entity structure review

- Quarterly estimated tax calculations

- Pricing: $2,400-$3,600 annually

Silver Tier – “Proactive Tax Advisory”

- Everything in Bronze, plus:

- Quarterly strategic planning meetings

- Multi-year tax projections (3 years)

- Retirement contribution optimization

- Expense optimization review

- Year-end planning session

- Pricing: $4,800-$7,200 annually

Gold Tier – “Comprehensive Tax Strategy”

- Everything in Silver, plus:

- Monthly advisory check-ins

- Entity restructuring analysis and implementation

- Cost segregation and depreciation planning

- Unlimited email and phone access

- CFO-level financial guidance integration

- Multi-entity planning and consolidation

- Pricing: $9,600-$15,000+ annually

Platinum Tier – “Family Office Tax Concierge”

- Everything in Gold, plus:

- Multi-generational wealth and estate planning

- Philanthropic giving strategies

- Investment portfolio tax optimization

- Business exit and succession planning

- Audit support and controversy assistance

- Pricing: $20,000-$50,000+ annually

Monthly Retainer vs. Project-Based Pricing

Monthly Retainer Advantages:

- Predictable revenue for practice cash flow

- Deeper client relationships and engagement

- Reduces price sensitivity and comparison shopping

- Encourages proactive communication from clients

- Higher lifetime client value

Project-Based Advantages:

- Easier to communicate value for specific deliverables

- Works well for transaction-specific planning (sale, restructuring)

- Less commitment is required from prospective clients

- Can supplement retainer services for additional work

Hybrid Approach (Recommended):

- Base retainer for ongoing advisory relationship

- Project fees for major initiatives (entity restructuring, cost segregation coordination)

- Clearly defined scope prevents scope creep

- Allows upselling additional services naturally

The Tax Planning Client Acquisition Funnel

Step 1: Target Market Identification

High-Value Client Profiles:

Successful Business Owners

- Revenue: $500K-$10M+ annually

- Current pain: Paying too much in taxes, seasonal cash flow challenges

- Buying trigger: Recent significant tax bill, business growth phase

Real Estate Investors

- Portfolio: 5+ properties or $2M+ in holdings

- Current pain: Managing depreciation, 1031 exchanges, entity structures

- Buying trigger: Property acquisition/disposition, portfolio expansion

High-Income Professionals

- Income: $250K-$1M+ (doctors, attorneys, executives, tech professionals)

- Current pain: AMT exposure, stock option planning, retirement optimization

- Buying trigger: Job change, equity event, income increase

Business Sellers Preparing for Exit

- Timeline: 2-5 years until transaction

- Current pain: Maximizing after-tax proceeds, succession planning

- Buying trigger: Received acquisition interest, retirement planning

Step 2: Educational Content Marketing

Blog Content Strategy (Target: 2-4 posts monthly)

Sample article topics:

- “7 Year-End Tax Strategies Every Business Owner Should Implement Before December 31”

- “How Cost Segregation Studies Can Save Real Estate Investors $100K+ in Taxes”

- “S-Corp vs. LLC: Which Entity Structure Minimizes Your Tax Bill?”

- “The Ultimate Guide to Maximizing Retirement Contributions for Business Owners”

Include internal links to:

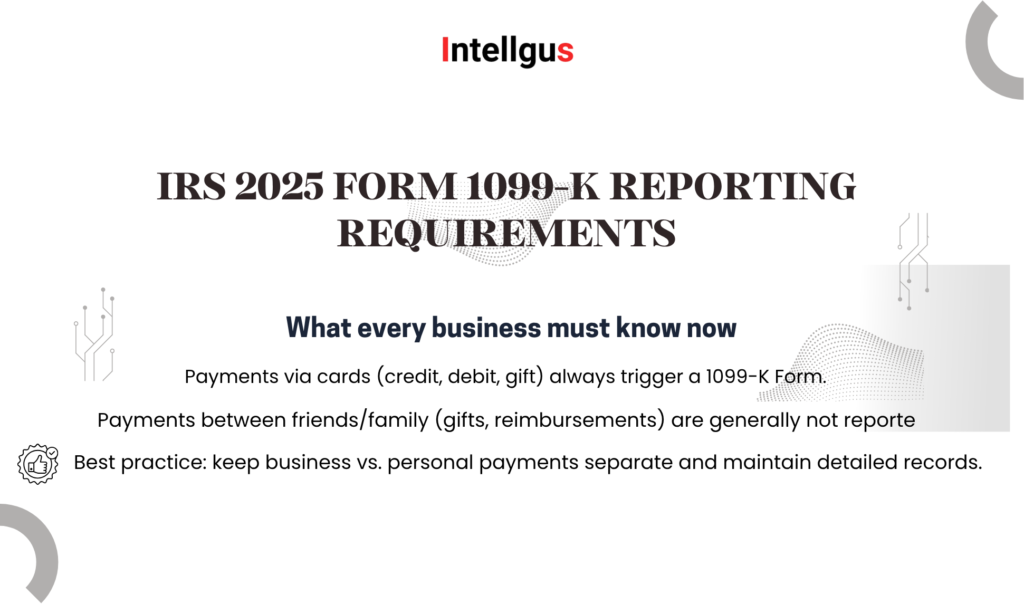

- Your firm’s IRS 1099-K compliance guide (related tax topic)

- Accounting practice transition services (for business owner readers)

- Client success stories and case studies (social proof)

Downloadable Lead Magnets:

Create valuable free resources requiring email opt-in:

- “2025 Tax Planning Checklist for Business Owners” (PDF)

- “Entity Structure Decision Matrix” (Interactive tool)

- “Quarterly Tax Planning Calendar” (Template)

- “Tax Deduction Maximizer Worksheet” (Spreadsheet)

Webinar and Workshop Series:

Monthly educational events:

- “Q4 Tax Planning Strategies Workshop” (October/November)

- “New Tax Law Updates for 2025” (January)

- “Real Estate Tax Planning Masterclass” (Quarterly)

- “Business Owner’s Guide to Proactive Tax Planning” (Monthly)

Step 3: Strategic Referral Partnerships

Complementary Professional Relationships:

Financial Advisors and Wealth Managers

- Natural fit: Tax planning integrates with investment management

- Value exchange: You provide tax expertise, they provide investment management

- Co-marketing opportunity: Joint client workshops and seminars

- Referral structure: Formalized reciprocal agreement

Attorneys (Estate, Business, Real Estate)

- Entity formation and restructuring coordination

- Estate planning implementation requiring tax analysis

- Business transaction legal work with tax implications

- M&A advisory requiring an integrated approach

Commercial Bankers and Lenders

- Business clients seeking financing need tax planning

- Cash flow optimization improves loan qualification

- Financial statement preparation and analysis

- Referral source for business banking customers

Insurance Professionals

- Life insurance tax planning integration

- Business succession funding strategies

- Disability and liability coverage for business owners

- Captive insurance planning (advanced strategy)

Referral Agreement Best Practices:

Formalize partnerships with written agreements:

- Define the ideal client profile that both parties serve

- Establish communication protocols and the introduction process

- Set expectations around response time and service quality

- Address confidentiality and professional standards

- Consider co-branded marketing materials

- Track referrals and maintain reciprocal relationships

Revenue Opportunity: Referral partnerships can generate 30-50% of new client acquisition

Step 4: Client Onboarding and Engagement Process

Initial Discovery Meeting (Complimentary)

60-90 minute consultation to:

- Understand the client’s financial situation and goals

- Review prior year tax returns (bring copies)

- Identify immediate planning opportunities

- Explain service offerings and pricing

- Assess cultural fit and working relationship

Comprehensive Tax Analysis (Paid Engagement)

Deep-dive review before ongoing relationship:

- Three-year historical tax return analysis

- Entity structure evaluation and recommendations

- Expense optimization audit

- Retirement planning assessment

- Multi-year projection development

- Written tax planning memo with prioritized recommendations

Fee: $1,200-$2,500 (credited toward annual retainer if client engages)

Formal Engagement and Service Agreement

Clear documentation including:

- Scope of services and deliverables

- Meeting frequency and communication expectations

- Pricing structure and payment terms

- Technology requirements (client portal, document sharing)

- Termination provisions

- Professional standards and limitations

Quarterly Strategic Planning Meetings

Structured agenda maximizing value:

- Pre-meeting: Client completes questionnaire about recent changes

- Meeting agenda:

- Review the prior quarter’s financial performance

- Update annual tax projection

- Identify planning opportunities and deadlines

- Review estimated tax obligation

- Assign action items with deadlines

- Post-meeting: Documented meeting summary and task list

Technology Stack for Efficient Tax Planning Delivery

Essential Software and Tools

Tax Planning and Projection Software

- Comprehensive scenario modeling

- Side-by-side strategy comparison

- Client-friendly presentation reports

- Integration with tax preparation software

- Pricing: $200-$400/month

Holistiplan

- Tax return analysis and planning tool

- Ideal for CPA-financial advisor collaboration

- Automated opportunity identification

- Client presentation materials

- Pricing: $99-$199/month

Practice Management and Client Portal

Canopy

- All-in-one practice management

- Client portal and document management

- Workflow automation and task management

- Time tracking and billing

- Pricing: $55-$105/user/month

- Client communication platform

- Secure messaging and file sharing

- Automated reminders and follow-ups

- Mobile app for client convenience

- Pricing: $30-$60/user/month

Financial Planning Integration

- Comprehensive financial planning

- Tax planning module integration

- Retirement and Social Security optimization

- Client collaboration tools

- Pricing: $100-$150/month

Document Management and Automation

- Cloud-based document storage

- Client portal functionality

- Automated workflows and organization

- Integration with tax software

- Pricing: $20-$40/user/month

Proposal and Engagement Letter Automation

Ignition (formerly Practice Ignition)

- Automated proposal generation

- Electronic engagement letter signing

- Payment processing and billing

- Subscription management

- Pricing: $59-$109/month

Overcoming Common Tax Planning Implementation Challenges

Challenge 1: “My Clients Only Want Tax Preparation, Not Planning”

Reality Check: Clients don’t know to ask for what they’ve never experienced.

Solutions:

Demonstrate Value Before Asking for Commitment

- Offer complimentary tax analysis during initial meeting

- Show specific dollar amount savings opportunities

- Present findings in a visual, easy-to-understand format

- Focus on pain points: “You paid $X unnecessarily last year—here’s how we prevent that”

Reframe the Conversation

- Stop selling “tax planning services”

- Start selling “keeping more of what you earn”

- Use before/after scenarios: “You paid $75K in taxes last year. With proactive planning, that could have been $52K. That’s $23K you could have kept.”

Start Small and Expand

- Begin with a limited planning scope (mid-year projection only)

- Demonstrate value through initial engagement

- Upsell comprehensive planning once trust is established

Challenge 2: “I Don’t Have Time to Add Planning Services”

Reality Check: Tax planning is more profitable per hour than preparation.

Solutions:

Leverage Technology

- Tax planning software reduces analysis time by 60-70%

- Automated projection templates eliminate manual calculations

- Client portals reduce administrative communication time

Systematize Service Delivery

- Create standardized meeting agendas and checklists

- Develop template deliverables and planning memos

- Use junior staff for data gathering and preliminary analysis

- Reserve senior time for strategy development and client meetings

Outsource Lower-Value Tasks

- Delegate data entry and bookkeeping

- Use offshore resources for return preparation

- Focus internal capacity on high-margin advisory work

Intellgus staffing solutions enable firms to:

- Offload compliance work to qualified professionals

- Free up senior staff capacity for advisory services

- Scale efficiently without full-time hiring commitments

- Maintain quality while improving profitability

Challenge 3: “Clients Don’t Want to Pay Advisory Fees”

Reality Check: Clients happily pay for value they understand.

Solutions:

Quantify ROI in Dollar Terms

- “This $5,000 planning engagement will save you $18,000 in taxes.”

- ROI: 260% return on investment

- Present as investment, not expense

Restructure Pricing Psychology

- Instead of: “$7,200 annual fee”

- Try: “$600/month investment that saves you $2,000/month in taxes”

- Monthly payment reduces sticker shock

- Emphasizes ongoing value, not a one-time purchase

Create Comparison Anchoring

- Show current state: “You’re paying $X to IRS annually”

- Present alternative: “With planning, you’d pay $Y—a difference of $Z”

- Emphasize: “Would you invest $A to save $B?”

Challenge 4: “I’m Not Confident in My Planning Skills”

Reality Check: Most CPAs underestimate their existing knowledge.

Solutions:

Start with Low-Complexity Strategies

- Entity structure optimization (S-corp elections)

- Retirement contribution maximization

- Expense documentation improvement

- Estimated tax planning

These strategies alone generate significant value and build confidence.

Invest in Continuing Education

Recommended resources:

- National Institute of Certified Tax Planners (NICTP) – Certification program

- The Tax Adviser (AICPA) – Monthly publication

- Tax Planning Institute by TaxBuzz – Online courses

- State CPA society tax conferences and workshops

Join Peer Learning Communities

- CPA Academy discussion forums

- Accountants Flight Plan mastermind groups

- Local CPA study groups focused on tax planning

- Online communities: Reddit r/taxpros, TaxProTalk

Engage Technical Consultants

- For complex situations beyond your expertise

- Technical tax research firms (KPMG, PwC, EY technical hotlines)

- Specialty consultants for niche areas (cost segregation, R&D credits, international tax)